Hard Price Bargaining over Kronos

Zohr Is Taking on Water and Millions of Dollars Are Being Lost. Against the Backdrop of Presidential Elections and the Turkish Threat

By Dr. Yiannos Charalambides

International Relations

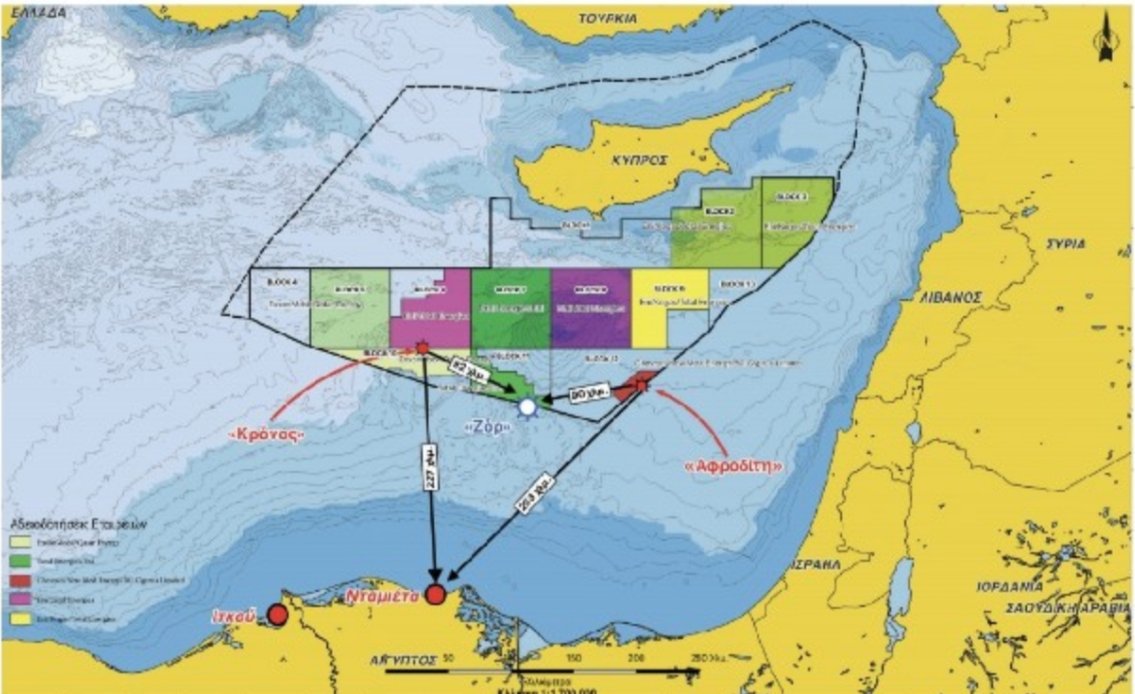

The Cypriot government is engaged in tough price negotiations with the companies ENI and TOTAL for the exploitation of the gas deposit in Block 6, namely “Kronos”.

Elections and the Turkish Threat

The bargaining does not depend solely on market rules, but also on other variables, such as:

- The timing of the signing of the agreement and the commencement of exploitation, which the government would like to take place around 2027, so as to constitute a strong weapon in President Christodoulides’ political arsenal for his re-election. (Estimates refer either to the end of 2027 or to 2028).

- Turkey’s stance. That is, whether it will introduce obstacles, even by creating a crisis. In strategic affairs, the actor with a legitimate interest is obliged to take into account all scenarios when facing Turkey, which, according to its claims, prioritises the defence of Turkish Cypriot rights and, particularly at this stage regarding natural gas, is raising the bar high. And it is issuing threats.

Credibility and Deterrence…

If, therefore, the President is in a hurry for the signing to take place before the end of his term, he becomes vulnerable in negotiations with the companies, which are not under the same pressure. If, on the other hand, he seeks to avoid any complication due to Turkish escalation of threats, then:

A) Either the signing will be postponed until after the elections, when there will be greater room for manoeuvre, or

B) deterrence support will have to be obtained from foreign actors — but from whom?

ENI has proven unreliable in the past. As for TOTAL, it is not certain whether France would clash with Turkey on our behalf. France has interests in Cyprus through TOTAL, but it also has interests in Ankara. As for the EU, given that it did not intervene in the Cyprus–Greece interconnection cable to deter Turkish threats near Kasos, how can one rely on it if something goes wrong with Ankara?

It is true that, regarding the cable issue, a diplomatic mistake was made, among others, because Athens framed it as a Greek–Turkish issue instead of, together with Nicosia, placing it before Brussels as a common, subsidised project. This would have meant adoption within the Council conclusions, implying that if Turkey provoked or escalated into a crisis, Article 42(7) of the Treaties could be activated.

Why are all these issues being emphasised? So that the government is prepared to prevent the worst and to realise the vision under the best possible terms.

The Mistakes at Zohr and the Loss of Millions

There is also a third factor that must be taken into account. The mistakes made at the Egyptian Zohr field and the losses suffered by ENI and TOTAL.

Zohr, which had been presented in celebratory terms, has “collapsed”, as one would say colloquially. At present it produces approximately 1.5–2.0 bcf/d (billion cubic feet per day), whereas in early 2020 it produced 2.7–3.0 bcf/d. The decline in production is striking, due to problems such as water ingress.

What does this mean? Due to water entering the reservoir, the well now produces natural gas together with water, which reduces net gas production and increases exploitation costs.

How did this occur? The Egyptians pressured the companies for rapid and large-scale exploitation that would generate substantial profits and cover approximately 20% of the country’s domestic needs. As a result, the high and rapid exploitation of a sensitive carbonate reservoir caused a sharp pressure drop, allowing water to move rapidly towards the wells, causing damage that, by conservative estimates, amounts to 10 million dollars per month.

The cost is not catastrophic, but it is a bleeding wound. Under these conditions, the original planning proved incorrect. This constitutes a lesson for the case of Kronos, which implies, among other things, the following:

- The same mistakes regarding the speed of production must not be repeated.

2. The price agreement must clearly be above breakeven.

3. There must be flexibility in the agreement if something goes wrong.

Kronos Enters the Game…

It is true that the companies would like to recover part of the costs they have incurred at Zohr through the negotiations they are conducting with Nicosia, in the sense that:

A) They constitute the most advantageous option, given that Cyprus lacks infrastructure and any alternative option would be of lesser benefit to Nicosia.

B) The government seeks to demonstrate tangible results and is therefore more vulnerable in negotiations.

The more time passes, the more vulnerable it becomes, especially if it sets a signing milestone before the elections.

Contracts and Price Determination

Where do we stand at present? Kronos is a medium-sized field, and Cyprus does not have its own infrastructure (3.1–3.4 trillion cubic feet of natural gas). Consequently, it must proceed with transporting the gas to Egypt, to Damietta, where liquefaction takes place and re-export follows to the global market, primarily to the EU, which is disengaging from Russia and requires — at least for the coming years — sources of natural gas, particularly from EU member states.

Of course, this dependence on foreign infrastructure means higher fees and lower net profit.

In essence, the prices that Kronos can deliver are not impressive. Therefore, the project can move forward only when the parties reach mutually beneficial prices.

Under the current conditions:

- The cost from Kronos to LNG at Damietta reaches 5.5–7 dollars per cubic meter of natural gas.

2. For the investment to be justified, the price must be above 7.5–8 dollars per cubic meter. This is an acceptable price. At 8–10 dollars it is very good, and above 10 dollars it is highly attractive.

In the negotiations, particularly regarding Kronos, the companies seek long-term contracts of approximately 10 to 15 years (sometimes 20), with prices determined as follows:

A) Indexed pricing, i.e. linked to a reference price index (for example Brent or hubs such as TTF and JKM).

How does the system work? The selling price of natural gas is not fixed and therefore follows a reference index such as Brent, the European gas exchange (TTF), or the Asian LNG price (JKM).

For example, the final price may be equal to 90% of the TTF price plus a small margin. If the reference index rises, the price rises accordingly, and vice versa.

B) Hybrid formula, which includes two reference prices. One is fixed (a safety amount) plus a reference index, which is variable.

For example, the fixed price may be 4 dollars, to which the variable Brent or TTF or JKM component is added, depending on what is decided.

C) Ceiling, meaning that the price cannot exceed a certain limit, such as 12 dollars.

D) Protection clauses, meaning that the price cannot fall below a certain threshold, such as 6 dollars.

E) Take or Pay, meaning “Take or Pay”, which means that either you take the agreed quantity and sell it or you pay for it anyway. In this way, revenue for the producer is ensured.

F) Destination clause, which determines where the natural gas will be sold — whether sales will be free or restricted to specific market(s).

“Derivatives”…

There is also another formula that could be included in the agreement. This concerns derivatives (“hedging”), meaning that within a horizon of 1 to 5 years, price insurance can be achieved using financial instruments in order to reduce the risks arising from price volatility. These instruments include the following:

- Futures (future price contracts). In other words, you lock in today a price for the future, agreeing to sell on a specific date at a specific price. There is protection if the market price falls, but there is a loss of any additional profit.

- Swaps (price swaps), meaning the exchange of floating for fixed prices. The state or the company determines that regardless of the market price, it wants, for example, 7.5 dollars. If the price falls below the fixed 7.5 dollars, there is no loss and the same price continues. If it rises, the additional profit is lost.

- Options (rights). One purchases a right, not an obligation. That is, one pays a small amount — a premium — for the right to sell at a minimum price, such as 7 dollars. If the price falls, the right is exercised. If the price rises, it is ignored and sales occur at the higher price.

Shares and Taxes…

Within the framework of the negotiations, one may ask what percentage Cyprus can obtain from Kronos. The percentage is a combination of the following parameters:

First, royalties on production. This is a fixed percentage paid to the state for every quantity of hydrocarbons produced, regardless of profitability. For example, 5%.

Second, corporate income tax, which is paid after costs and depreciation are deducted. In this context, bargaining takes place regarding the percentage paid by the company on net profits.

Under these conditions, the state assumes the initial risk, exchanging it, for example, for accelerated procedures — for political reasons such as elections. In the early years, income tax may be low or zero, and companies usually bargain hard. According to information, ENI and TOTAL are exerting pressure on this matter.

On the other hand, the state may demand higher revenues over the long term. However, it bears the initial risk in such an agreement.

Taking into account what happens in similar cases, Cyprus could secure a long-term share of up to 25%, on a graduated basis, given that it does not have its own infrastructure and given that Kronos is not a gold mine but a fairly profitable project.

Usually these stages are graduated. That is, they concern the early years with high risk, with the share ranging from 10% to 15%, followed by the middle phase with 15% to 20%, and the third, mature phase, which may range from 20% to 25%. The average may range from 18% to 22%.

When reference is made to “share”, it concerns the percentage of revenues or profits received by each side. The state’s share derives from royalties and taxes, while companies’ shares derive from net profits.

Transparency and the President

Caution is therefore required in the bargaining. If the President seeks to gain time due to elections, companies will logically — if they play on long-term profits — use this as his disadvantage and their advantage for greater gains.

Transparency, therefore, is necessary — both for the President’s image and for the good of the country.